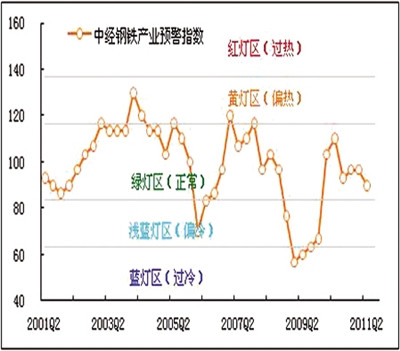

The warning sign of the warning sign of the China Railway Economic Industry is based on the way of traffic lights to distinguish the status of some important indicators describing the development of the industry: red light means too fast (overheating), yellow light means too fast (bias Hot), the green light indicates normal stability, the light blue light indicates slow (cold), the blue light indicates too slow (too cold); the individual indicator values ​​assigned to different indicator lights are combined, and the comprehensive early warning index is also summarized. Also displayed by 5 light zones, the meaning is the same as above. .jpg)

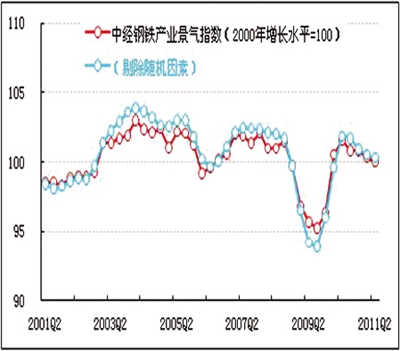

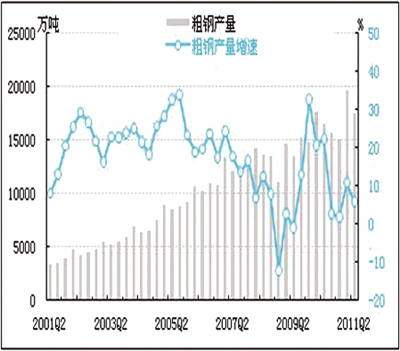

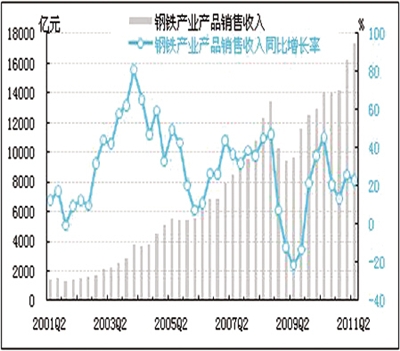

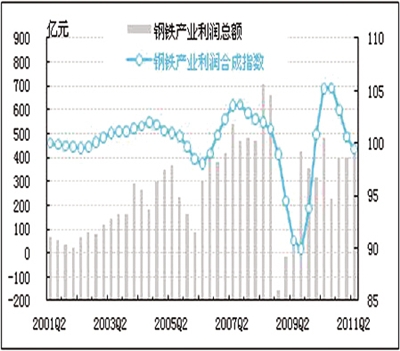

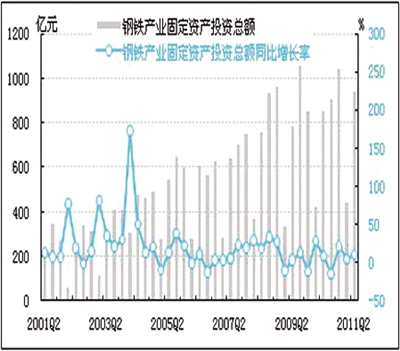

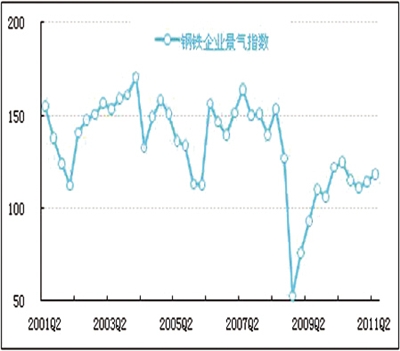

The core content industry maintained a stable operation. The growth rate of production and sales slowed down. The overall operation of the steel industry in the second quarter was relatively stable. According to the report of the China Economic and Steel Industry Climate Index, in the second quarter of 2011, the China Economic and Steel Industry Climate Index was 100.1 points, a slight decrease of 0.2 points from the previous quarter; the China Railway Steel Industry Early Warning Index was 90.0 points, down 6.7 points from the previous quarter. Affected by factors such as relatively sluggish domestic and international market demand, the growth rate of production and sales in the steel industry slowed down in the second quarter, steel product prices fluctuated downward, and the profitability of the steel industry was at a low level. The operation of the steel industry needs to stabilize. In the third quarter of 2011, the situation facing the development of the steel industry is more complicated. Affected by the domestic and international demand situation, China's steel industry may face the situation of poor steel sales and the resulting weak steel prices. At the same time, the high price of iron ore has also severely squeezed the profit margin of the steel industry. It is expected that China's steel industry will continue to maintain a moderate decline in the third quarter, and may enter the "destocking" channel. At present, the problem of low efficiency in the steel industry needs to be highly valued and resolved. The steel industry should fully understand the changes in the international and domestic markets, implement the requirements for controlling the total amount of steel production and total steel production capacity, and shift the focus of work to accelerating the transformation of development mode and structural adjustment, and continuously improve the quality and efficiency of industry development. Actively promote the merger and reorganization of steel enterprises and energy conservation and emission reduction work, and strive to promote the steady and healthy development of the steel industry. The industry boom slowly slowed down : In the second quarter of 2011, the China Economic and Steel Industry 1 prosperity index was 100.1 points (2000 growth level = 10,002), a slight decrease of 0.2 points from the previous quarter. Among the six indicators that constitute the China Steel Industry Climate Index (excluding seasonal factors 4 and the retention of random factors 5), the export volume of steel industry and the total investment in fixed assets have increased, the number of employees, total profit, product sales revenue and The total amount of tax (speed growth) has dropped to varying degrees. After further eliminating the random factors, the China Economic and Steel Industry Climate Index is 100.3 points (see the blue curve in the China Economic and Steel Industry Boom Chart), which is 0.2 points lower than the previous quarter and 0.2 points higher than the sentiment index without removing the random factors. This indicates that the steel industry's own growth momentum has increased, and random factors such as extreme weather and related industry policy changes have a certain pull-down effect on the steel industry. Early warning: In the second quarter of 2011, the early warning index of the China Iron and Steel Industry was 90.0 points, down 6.7 points from the previous quarter. It continued to converge under the center line of the “Green Light†area for four quarters, indicating that the development of the steel industry was initially involved in “bottlenecksâ€. It is still waiting for further stabilization. Light: In the second quarter of 2011, among the 10 indicators that constitute the early warning index of the China Steel Industry (excluding seasonal factors, retaining random factors), there is one indicator in the “Yellow Light District†– the steel industry producers leave the factory. Price index; there are 6 indicators in the "Green Light District" - total investment in fixed assets of the steel industry, steel exports, sales revenue of steel industry products, number of employees in the steel industry, accounts receivable in the steel industry (reversed 6) and steel The capital of industrial finished products is occupied (reversed); there are two indicators in the “light blue light district†– the total tax revenue of the steel industry and the profit synthesis index of the steel industry; there is one indicator in the “blue light district†– crude steel output . Comparing with the previous quarter's light map, it can be seen that one of the 10 indicators in this quarter has risen by 1 light, 6 indicators are unchanged, and 3 indicators are down by 1 light. Major indicators slowed down production: a small decline In the second quarter of 2011, under the influence of the weakening of overall demand for downstream manufacturing industries such as automobiles and home appliances, the growth rate of production and sales of the steel industry slowed down. After the preliminary seasonal adjustment, in the second quarter of 2011, China's crude steel output was 1,761,680 tons, up 6.1% year-on-year. The year-on-year growth rate was 4.8 percentage points slower than the previous quarter; the chain growth rate was -10.6%, while the previous quarter was a quarter-on-quarter growth. 30.0%. Sales: growth rate decline In the second quarter of 2011, China's steel industry product sales revenue was 1,738.77 billion yuan, a year-on-year increase of 23.0%, the growth rate slowed by 3.0 percentage points from the previous quarter; the chain rose by 6.7%, the growth rate slowed down from the previous quarter by 8.1 percentage point. Inventory: growth slowed down in the second quarter of 2011, due to the decline in raw material iron ore prices, the steel export situation is weakening, and in the downstream industry, the demand for steel products will continue to weaken, the growth rate of finished steel products in the steel industry has been released. Slow, may start a new round of destocking process. As of the end of the second quarter of 2011, the capital occupation of finished steel products was 226.55 billion yuan, a year-on-year increase of 18.2%, and the growth rate slowed by 6.5 percentage points from the previous quarter. Exports: Continued Weakness Recently, the pace of economic recovery in the United States has slowed down, the overseas steel market is in a downturn, and international steel prices are declining. At the same time, due to the rising average price of steel exports, domestic and international spreads have shrunk, and China’s steel exports are in a weak state. The proportion of production continued to decline. After preliminary seasonal adjustment, the export value of steel in the second quarter of 2011 was US$14.56 billion, a year-on-year increase of 48.5%. The year-on-year growth rate was 11.7 percentage points higher than the previous quarter; the chain growth was 42.1%, and the growth rate was 21.6 percentage points higher than the previous quarter. The export growth rate was significantly accelerated by the base. Since mid-June, the domestic steel market has shifted from a narrow range to a full-line decline, and the market has a strong wait-and-see atmosphere. It is expected that downstream demand will remain sluggish in the next few months. The domestic steel market will remain weak, or it will drive down the international steel market. As a result, the domestic and international spreads may continue to narrow, which will inevitably inhibit steel exports. China's steel export situation is still grim. Ex-factory price: downward fluctuation On the one hand, the international steel market is in the downward channel, the domestic steel market maintains a shock consolidation pattern, and the effective demand is weakened. On the other hand, although the growth rate of crude steel production has declined somewhat, it is still at a high level. The basic situation has not changed. Driven by the above factors, in the second quarter of 2011, the ex-factory price of producers in the steel industry rose by 9.5% year-on-year, and the growth rate dropped by 8.2 percentage points from the previous quarter. At present, the situation of iron ore pressure is serious, and there is a downside in the cost of the steel industry. It is expected that domestic steel prices will continue to fall in the third quarter. Profit: low level In the quarter, although China's iron ore import price has declined, it has reduced the profit pressure of the steel industry to a certain extent, but the role of the steel industry's product price and price decline is the dominant factor, making the steel industry profitability level. Reduced. After preliminary seasonal adjustment, the total profit of the steel industry in the second quarter of 2011 was 41.89 billion yuan, a year-on-year growth rate of -13.6%, compared with a year-on-year increase of 25.3%; the chain growth was 5.1%, and the growth rate of the chain was slightly higher than the previous quarter by 3.6. percentage point. The profit margin of the steel industry maintained 2.4% in the previous quarter, far below the national industrial sales profit rate of 6.2%. It is the least profitable industry in China's major industries except oil processing, coking and nuclear fuel processing. Loss: still large and adjusted by the initial season. In the second quarter of 2011, the loss of the loss-making enterprises in the steel industry totaled 5.37 billion yuan, a decrease of 1.99 billion yuan from the previous quarter and an increase of 2.48 billion yuan over the same period of last year. The loss was down from 20.9% in the previous quarter. This quarter's 20.2% is still significantly higher than the 13.5% loss level of all industries. Taxation: Apparently falling back In the second quarter of 2011, the profitability of the steel industry declined, driving the growth rate of total tax revenue to decline. After the initial seasonal adjustment, the total tax revenue of the steel industry in the second quarter of 2011 was 27.87 billion yuan, a year-on-year increase of 0.9%. The year-on-year growth rate slowed down by 23.9 percentage points from the previous quarter; the chain growth rate was -23.3%, and the previous quarter was a year-on-year increase of 24.4. %. According to estimates, random factors have driven the tax expenditure on the steel industry to reduce by 940 million yuan. Employment: Slower growth As the growth rate of steel industry production and sales slows down, steel prices fall, profitability declines, and employment growth in the steel industry slows down. In the second quarter of 2011, the number of employees in the steel industry was 3.208 million, an increase from the previous quarter; the number of employees increased by 6.6% year-on-year, and the growth rate was 0.9 percentage points lower than that of the previous quarter, but still lower than the average industrial scale above the scale. 10.6% growth rate. Investment: The low recovery was driven by the still-increasing urban fixed asset investment. After the initial seasonal adjustment, the fixed assets investment of the steel industry in the second quarter of 2011 was 94.16 billion yuan, a year-on-year increase of 10.5%, and the growth rate was 5.7 percentage points higher than the previous quarter. It is still at a historical low; the chain increased by 111.6%, and the growth rate of the previous quarter was -57.2%. Accounts receivable: continue to improve In the second quarter of 2011, the net receivables of the steel industry was RMB 20.38 billion, a year-on-year increase of 20.2%, and the year-on-year growth rate decreased by 6.3 percentage points from the previous quarter. After calculation, the quarterly receivables turnover days decreased from 10.9 days in the previous quarter to 10.0 days in the current quarter, and the capital turnover continued to improve, and was significantly better than the average turnover days of all industrial 28.5 days of accounts receivable. It shows that the steel industry's asset flow is accelerating and its solvency is further enhanced. Business climate: relatively stable In the second quarter of 2011, the steel industry's prosperity index was 118.5, up 4.3 points from the previous quarter, maintaining the momentum of the last quarter. This shows that steel companies have a relatively stable confidence in the prospects of the steel industry. Industry expectations and recommendations Overall, the current steel industry market demand tends to be sluggish, the steel industry's production and sales growth rate has slowed down, steel product prices fluctuated downward, the steel industry profitability level is at a low level, and steel companies' losses have increased significantly compared with the same period last year. Iron and steel enterprises are also at a relatively high level in the industrial sector, and steel companies are cautious about employment. However, under the overall investment of the whole society, the investment growth rate of the steel industry has rebounded at a low level, and the rate of collection of accounts receivable has continued to accelerate. In the third quarter of 2011, the situation facing the development of the steel industry is more complicated. First, strategic emerging industry investment and other people's livelihood projects have a positive effect on investment, while real estate control measures have inhibited the growth of investment to a certain extent, so investment factors may show a moderate decline. Secondly, the growth rate of consumption of household appliances, automobiles and other products has declined, which has had a certain impact on the growth of manufacturing industries such as automobiles and machinery. With the arrival of the traditional low demand for steel products, the pattern of weak operation in the domestic steel market will be difficult to change in the short term. Thirdly, from the perspective of the external demand market, the steel demand for post-disaster reconstruction in Japan is first driven by the increase in capacity utilization rate in Japan (the capacity utilization rate in Japan before the earthquake is not high), and the scale and progress of reconstruction will affect the foreign steel. Demand, Japan's post-disaster reconstruction may not have a significant impact on China's steel exports; Europe and the United States gradually entered a seasonal summer break, market demand into a dull period. From the micro survey of some steel mills, the export orders for steel from Europe have decreased significantly since May, and some steel mills have zero orders for Europe in June. In addition, the cumulative effect of raising the reserve ratio and raising interest rates has appeared for some time. High financing costs not only affect steel companies, but also affect the investment and production of steel downstream enterprises. Affected by the domestic and international demand situation, China's steel industry may face the situation of poor steel sales and the resulting steel prices are weak, and iron ore prices continue to fall, it is expected to expand the profitability of steel companies. In general, China's steel industry is expected to maintain a moderate decline in the third quarter of 2011, and may step into the “destocking†channel. In the face of complex situations, the steel industry should respond to the following aspects: First, steel companies should pay close attention to market trends and timely adjust and optimize iron ore procurement strategies. When purchasing iron ore, appropriately adjust the proportion of domestic and foreign mineral materials, and more comprehensively consider the factors affecting the iron ore market, and try to control the rhythm of the price of minerals to minimize the cost. Second, iron and steel enterprises should actively participate in the observation of market trends, and try to participate in futures and spot transactions at the same time, in order to make up for losses through the recent market complementarity. In addition, the pattern of the domestic steel distribution industry is changing. Steel companies should try to extend the service chain and do deep processing to meet the diversified and personalized needs of customers. Third, iron and steel enterprises should speed up the "going out" pace, better use of "two markets" and "two kinds of resources" will become an inevitable choice for China's steel industry to further enhance resource support capabilities and international competitiveness. In the process of development, China's steel enterprises should pay more and more attention to the establishment of factories in areas with resources and markets overseas. Conditional enterprises should regard overseas layout as an important part of corporate strategic development. At the same time, the export of high-end products and services should be replaced by the export of low-end products. Notes: 1 The steel industry refers to the ferrous metal smelting and rolling processing industry in the national economic industry classification. The statistical scope of this report is nearly 6,400 industrial enterprises above designated size in the industry. In 22000, the warning signs of the steel industry were basically in the green light area, which was relatively stable, so it was set as the base year of the China Economic and Steel Industry Climate Index. 3 According to the calculation method of the climate warning index system, the composition indicators of the industry prosperity index and the industry early warning index should be adjusted seasonally to eliminate the influence of seasonal factors on the data. Therefore, when the industry climate index and early warning index release the current data, the previous data will also be adjusted. . 4 Seasonal factors refer to the impact of seasonal changes on the data. For example, the market sales of cold drinks vary with the temperature of the four seasons year after year. 5 Random factors are also called irregularities, such as the impact of new policy implementation, macro-control, natural disasters and other factors on the data. 6 Reversal indicators, also called reverse indicators, have a negative effect on the industry's operating conditions. The lower the indicator value, the better the industry situation, and vice versa. 7 Preliminary seasonal adjustment refers to only eliminating the influence of holiday factors such as the Spring Festival, and does not remove the influence of irregular factors.

The core content industry maintained a stable operation. The growth rate of production and sales slowed down. The overall operation of the steel industry in the second quarter was relatively stable. According to the report of the China Economic and Steel Industry Climate Index, in the second quarter of 2011, the China Economic and Steel Industry Climate Index was 100.1 points, a slight decrease of 0.2 points from the previous quarter; the China Railway Steel Industry Early Warning Index was 90.0 points, down 6.7 points from the previous quarter. Affected by factors such as relatively sluggish domestic and international market demand, the growth rate of production and sales in the steel industry slowed down in the second quarter, steel product prices fluctuated downward, and the profitability of the steel industry was at a low level. The operation of the steel industry needs to stabilize. In the third quarter of 2011, the situation facing the development of the steel industry is more complicated. Affected by the domestic and international demand situation, China's steel industry may face the situation of poor steel sales and the resulting weak steel prices. At the same time, the high price of iron ore has also severely squeezed the profit margin of the steel industry. It is expected that China's steel industry will continue to maintain a moderate decline in the third quarter, and may enter the "destocking" channel. At present, the problem of low efficiency in the steel industry needs to be highly valued and resolved. The steel industry should fully understand the changes in the international and domestic markets, implement the requirements for controlling the total amount of steel production and total steel production capacity, and shift the focus of work to accelerating the transformation of development mode and structural adjustment, and continuously improve the quality and efficiency of industry development. Actively promote the merger and reorganization of steel enterprises and energy conservation and emission reduction work, and strive to promote the steady and healthy development of the steel industry. The industry boom slowly slowed down : In the second quarter of 2011, the China Economic and Steel Industry 1 prosperity index was 100.1 points (2000 growth level = 10,002), a slight decrease of 0.2 points from the previous quarter. Among the six indicators that constitute the China Steel Industry Climate Index (excluding seasonal factors 4 and the retention of random factors 5), the export volume of steel industry and the total investment in fixed assets have increased, the number of employees, total profit, product sales revenue and The total amount of tax (speed growth) has dropped to varying degrees. After further eliminating the random factors, the China Economic and Steel Industry Climate Index is 100.3 points (see the blue curve in the China Economic and Steel Industry Boom Chart), which is 0.2 points lower than the previous quarter and 0.2 points higher than the sentiment index without removing the random factors. This indicates that the steel industry's own growth momentum has increased, and random factors such as extreme weather and related industry policy changes have a certain pull-down effect on the steel industry. Early warning: In the second quarter of 2011, the early warning index of the China Iron and Steel Industry was 90.0 points, down 6.7 points from the previous quarter. It continued to converge under the center line of the “Green Light†area for four quarters, indicating that the development of the steel industry was initially involved in “bottlenecksâ€. It is still waiting for further stabilization. Light: In the second quarter of 2011, among the 10 indicators that constitute the early warning index of the China Steel Industry (excluding seasonal factors, retaining random factors), there is one indicator in the “Yellow Light District†– the steel industry producers leave the factory. Price index; there are 6 indicators in the "Green Light District" - total investment in fixed assets of the steel industry, steel exports, sales revenue of steel industry products, number of employees in the steel industry, accounts receivable in the steel industry (reversed 6) and steel The capital of industrial finished products is occupied (reversed); there are two indicators in the “light blue light district†– the total tax revenue of the steel industry and the profit synthesis index of the steel industry; there is one indicator in the “blue light district†– crude steel output . Comparing with the previous quarter's light map, it can be seen that one of the 10 indicators in this quarter has risen by 1 light, 6 indicators are unchanged, and 3 indicators are down by 1 light. Major indicators slowed down production: a small decline In the second quarter of 2011, under the influence of the weakening of overall demand for downstream manufacturing industries such as automobiles and home appliances, the growth rate of production and sales of the steel industry slowed down. After the preliminary seasonal adjustment, in the second quarter of 2011, China's crude steel output was 1,761,680 tons, up 6.1% year-on-year. The year-on-year growth rate was 4.8 percentage points slower than the previous quarter; the chain growth rate was -10.6%, while the previous quarter was a quarter-on-quarter growth. 30.0%. Sales: growth rate decline In the second quarter of 2011, China's steel industry product sales revenue was 1,738.77 billion yuan, a year-on-year increase of 23.0%, the growth rate slowed by 3.0 percentage points from the previous quarter; the chain rose by 6.7%, the growth rate slowed down from the previous quarter by 8.1 percentage point. Inventory: growth slowed down in the second quarter of 2011, due to the decline in raw material iron ore prices, the steel export situation is weakening, and in the downstream industry, the demand for steel products will continue to weaken, the growth rate of finished steel products in the steel industry has been released. Slow, may start a new round of destocking process. As of the end of the second quarter of 2011, the capital occupation of finished steel products was 226.55 billion yuan, a year-on-year increase of 18.2%, and the growth rate slowed by 6.5 percentage points from the previous quarter. Exports: Continued Weakness Recently, the pace of economic recovery in the United States has slowed down, the overseas steel market is in a downturn, and international steel prices are declining. At the same time, due to the rising average price of steel exports, domestic and international spreads have shrunk, and China’s steel exports are in a weak state. The proportion of production continued to decline. After preliminary seasonal adjustment, the export value of steel in the second quarter of 2011 was US$14.56 billion, a year-on-year increase of 48.5%. The year-on-year growth rate was 11.7 percentage points higher than the previous quarter; the chain growth was 42.1%, and the growth rate was 21.6 percentage points higher than the previous quarter. The export growth rate was significantly accelerated by the base. Since mid-June, the domestic steel market has shifted from a narrow range to a full-line decline, and the market has a strong wait-and-see atmosphere. It is expected that downstream demand will remain sluggish in the next few months. The domestic steel market will remain weak, or it will drive down the international steel market. As a result, the domestic and international spreads may continue to narrow, which will inevitably inhibit steel exports. China's steel export situation is still grim. Ex-factory price: downward fluctuation On the one hand, the international steel market is in the downward channel, the domestic steel market maintains a shock consolidation pattern, and the effective demand is weakened. On the other hand, although the growth rate of crude steel production has declined somewhat, it is still at a high level. The basic situation has not changed. Driven by the above factors, in the second quarter of 2011, the ex-factory price of producers in the steel industry rose by 9.5% year-on-year, and the growth rate dropped by 8.2 percentage points from the previous quarter. At present, the situation of iron ore pressure is serious, and there is a downside in the cost of the steel industry. It is expected that domestic steel prices will continue to fall in the third quarter. Profit: low level In the quarter, although China's iron ore import price has declined, it has reduced the profit pressure of the steel industry to a certain extent, but the role of the steel industry's product price and price decline is the dominant factor, making the steel industry profitability level. Reduced. After preliminary seasonal adjustment, the total profit of the steel industry in the second quarter of 2011 was 41.89 billion yuan, a year-on-year growth rate of -13.6%, compared with a year-on-year increase of 25.3%; the chain growth was 5.1%, and the growth rate of the chain was slightly higher than the previous quarter by 3.6. percentage point. The profit margin of the steel industry maintained 2.4% in the previous quarter, far below the national industrial sales profit rate of 6.2%. It is the least profitable industry in China's major industries except oil processing, coking and nuclear fuel processing. Loss: still large and adjusted by the initial season. In the second quarter of 2011, the loss of the loss-making enterprises in the steel industry totaled 5.37 billion yuan, a decrease of 1.99 billion yuan from the previous quarter and an increase of 2.48 billion yuan over the same period of last year. The loss was down from 20.9% in the previous quarter. This quarter's 20.2% is still significantly higher than the 13.5% loss level of all industries. Taxation: Apparently falling back In the second quarter of 2011, the profitability of the steel industry declined, driving the growth rate of total tax revenue to decline. After the initial seasonal adjustment, the total tax revenue of the steel industry in the second quarter of 2011 was 27.87 billion yuan, a year-on-year increase of 0.9%. The year-on-year growth rate slowed down by 23.9 percentage points from the previous quarter; the chain growth rate was -23.3%, and the previous quarter was a year-on-year increase of 24.4. %. According to estimates, random factors have driven the tax expenditure on the steel industry to reduce by 940 million yuan. Employment: Slower growth As the growth rate of steel industry production and sales slows down, steel prices fall, profitability declines, and employment growth in the steel industry slows down. In the second quarter of 2011, the number of employees in the steel industry was 3.208 million, an increase from the previous quarter; the number of employees increased by 6.6% year-on-year, and the growth rate was 0.9 percentage points lower than that of the previous quarter, but still lower than the average industrial scale above the scale. 10.6% growth rate. Investment: The low recovery was driven by the still-increasing urban fixed asset investment. After the initial seasonal adjustment, the fixed assets investment of the steel industry in the second quarter of 2011 was 94.16 billion yuan, a year-on-year increase of 10.5%, and the growth rate was 5.7 percentage points higher than the previous quarter. It is still at a historical low; the chain increased by 111.6%, and the growth rate of the previous quarter was -57.2%. Accounts receivable: continue to improve In the second quarter of 2011, the net receivables of the steel industry was RMB 20.38 billion, a year-on-year increase of 20.2%, and the year-on-year growth rate decreased by 6.3 percentage points from the previous quarter. After calculation, the quarterly receivables turnover days decreased from 10.9 days in the previous quarter to 10.0 days in the current quarter, and the capital turnover continued to improve, and was significantly better than the average turnover days of all industrial 28.5 days of accounts receivable. It shows that the steel industry's asset flow is accelerating and its solvency is further enhanced. Business climate: relatively stable In the second quarter of 2011, the steel industry's prosperity index was 118.5, up 4.3 points from the previous quarter, maintaining the momentum of the last quarter. This shows that steel companies have a relatively stable confidence in the prospects of the steel industry. Industry expectations and recommendations Overall, the current steel industry market demand tends to be sluggish, the steel industry's production and sales growth rate has slowed down, steel product prices fluctuated downward, the steel industry profitability level is at a low level, and steel companies' losses have increased significantly compared with the same period last year. Iron and steel enterprises are also at a relatively high level in the industrial sector, and steel companies are cautious about employment. However, under the overall investment of the whole society, the investment growth rate of the steel industry has rebounded at a low level, and the rate of collection of accounts receivable has continued to accelerate. In the third quarter of 2011, the situation facing the development of the steel industry is more complicated. First, strategic emerging industry investment and other people's livelihood projects have a positive effect on investment, while real estate control measures have inhibited the growth of investment to a certain extent, so investment factors may show a moderate decline. Secondly, the growth rate of consumption of household appliances, automobiles and other products has declined, which has had a certain impact on the growth of manufacturing industries such as automobiles and machinery. With the arrival of the traditional low demand for steel products, the pattern of weak operation in the domestic steel market will be difficult to change in the short term. Thirdly, from the perspective of the external demand market, the steel demand for post-disaster reconstruction in Japan is first driven by the increase in capacity utilization rate in Japan (the capacity utilization rate in Japan before the earthquake is not high), and the scale and progress of reconstruction will affect the foreign steel. Demand, Japan's post-disaster reconstruction may not have a significant impact on China's steel exports; Europe and the United States gradually entered a seasonal summer break, market demand into a dull period. From the micro survey of some steel mills, the export orders for steel from Europe have decreased significantly since May, and some steel mills have zero orders for Europe in June. In addition, the cumulative effect of raising the reserve ratio and raising interest rates has appeared for some time. High financing costs not only affect steel companies, but also affect the investment and production of steel downstream enterprises. Affected by the domestic and international demand situation, China's steel industry may face the situation of poor steel sales and the resulting steel prices are weak, and iron ore prices continue to fall, it is expected to expand the profitability of steel companies. In general, China's steel industry is expected to maintain a moderate decline in the third quarter of 2011, and may step into the “destocking†channel. In the face of complex situations, the steel industry should respond to the following aspects: First, steel companies should pay close attention to market trends and timely adjust and optimize iron ore procurement strategies. When purchasing iron ore, appropriately adjust the proportion of domestic and foreign mineral materials, and more comprehensively consider the factors affecting the iron ore market, and try to control the rhythm of the price of minerals to minimize the cost. Second, iron and steel enterprises should actively participate in the observation of market trends, and try to participate in futures and spot transactions at the same time, in order to make up for losses through the recent market complementarity. In addition, the pattern of the domestic steel distribution industry is changing. Steel companies should try to extend the service chain and do deep processing to meet the diversified and personalized needs of customers. Third, iron and steel enterprises should speed up the "going out" pace, better use of "two markets" and "two kinds of resources" will become an inevitable choice for China's steel industry to further enhance resource support capabilities and international competitiveness. In the process of development, China's steel enterprises should pay more and more attention to the establishment of factories in areas with resources and markets overseas. Conditional enterprises should regard overseas layout as an important part of corporate strategic development. At the same time, the export of high-end products and services should be replaced by the export of low-end products. Notes: 1 The steel industry refers to the ferrous metal smelting and rolling processing industry in the national economic industry classification. The statistical scope of this report is nearly 6,400 industrial enterprises above designated size in the industry. In 22000, the warning signs of the steel industry were basically in the green light area, which was relatively stable, so it was set as the base year of the China Economic and Steel Industry Climate Index. 3 According to the calculation method of the climate warning index system, the composition indicators of the industry prosperity index and the industry early warning index should be adjusted seasonally to eliminate the influence of seasonal factors on the data. Therefore, when the industry climate index and early warning index release the current data, the previous data will also be adjusted. . 4 Seasonal factors refer to the impact of seasonal changes on the data. For example, the market sales of cold drinks vary with the temperature of the four seasons year after year. 5 Random factors are also called irregularities, such as the impact of new policy implementation, macro-control, natural disasters and other factors on the data. 6 Reversal indicators, also called reverse indicators, have a negative effect on the industry's operating conditions. The lower the indicator value, the better the industry situation, and vice versa. 7 Preliminary seasonal adjustment refers to only eliminating the influence of holiday factors such as the Spring Festival, and does not remove the influence of irregular factors.

The core content industry maintained a stable operation. The growth rate of production and sales slowed down. The overall operation of the steel industry in the second quarter was relatively stable. According to the report of the China Economic and Steel Industry Climate Index, in the second quarter of 2011, the China Economic and Steel Industry Climate Index was 100.1 points, a slight decrease of 0.2 points from the previous quarter; the China Railway Steel Industry Early Warning Index was 90.0 points, down 6.7 points from the previous quarter. Affected by factors such as relatively sluggish domestic and international market demand, the growth rate of production and sales in the steel industry slowed down in the second quarter, steel product prices fluctuated downward, and the profitability of the steel industry was at a low level. The operation of the steel industry needs to stabilize. In the third quarter of 2011, the situation facing the development of the steel industry is more complicated. Affected by the domestic and international demand situation, China's steel industry may face the situation of poor steel sales and the resulting weak steel prices. At the same time, the high price of iron ore has also severely squeezed the profit margin of the steel industry. It is expected that China's steel industry will continue to maintain a moderate decline in the third quarter, and may enter the "destocking" channel. At present, the problem of low efficiency in the steel industry needs to be highly valued and resolved. The steel industry should fully understand the changes in the international and domestic markets, implement the requirements for controlling the total amount of steel production and total steel production capacity, and shift the focus of work to accelerating the transformation of development mode and structural adjustment, and continuously improve the quality and efficiency of industry development. Actively promote the merger and reorganization of steel enterprises and energy conservation and emission reduction work, and strive to promote the steady and healthy development of the steel industry. The industry boom slowly slowed down : In the second quarter of 2011, the China Economic and Steel Industry 1 prosperity index was 100.1 points (2000 growth level = 10,002), a slight decrease of 0.2 points from the previous quarter. Among the six indicators that constitute the China Steel Industry Climate Index (excluding seasonal factors 4 and the retention of random factors 5), the export volume of steel industry and the total investment in fixed assets have increased, the number of employees, total profit, product sales revenue and The total amount of tax (speed growth) has dropped to varying degrees. After further eliminating the random factors, the China Economic and Steel Industry Climate Index is 100.3 points (see the blue curve in the China Economic and Steel Industry Boom Chart), which is 0.2 points lower than the previous quarter and 0.2 points higher than the sentiment index without removing the random factors. This indicates that the steel industry's own growth momentum has increased, and random factors such as extreme weather and related industry policy changes have a certain pull-down effect on the steel industry. Early warning: In the second quarter of 2011, the early warning index of the China Iron and Steel Industry was 90.0 points, down 6.7 points from the previous quarter. It continued to converge under the center line of the “Green Light†area for four quarters, indicating that the development of the steel industry was initially involved in “bottlenecksâ€. It is still waiting for further stabilization. Light: In the second quarter of 2011, among the 10 indicators that constitute the early warning index of the China Steel Industry (excluding seasonal factors, retaining random factors), there is one indicator in the “Yellow Light District†– the steel industry producers leave the factory. Price index; there are 6 indicators in the "Green Light District" - total investment in fixed assets of the steel industry, steel exports, sales revenue of steel industry products, number of employees in the steel industry, accounts receivable in the steel industry (reversed 6) and steel The capital of industrial finished products is occupied (reversed); there are two indicators in the “light blue light district†– the total tax revenue of the steel industry and the profit synthesis index of the steel industry; there is one indicator in the “blue light district†– crude steel output . Comparing with the previous quarter's light map, it can be seen that one of the 10 indicators in this quarter has risen by 1 light, 6 indicators are unchanged, and 3 indicators are down by 1 light. Major indicators slowed down production: a small decline In the second quarter of 2011, under the influence of the weakening of overall demand for downstream manufacturing industries such as automobiles and home appliances, the growth rate of production and sales of the steel industry slowed down. After the preliminary seasonal adjustment, in the second quarter of 2011, China's crude steel output was 1,761,680 tons, up 6.1% year-on-year. The year-on-year growth rate was 4.8 percentage points slower than the previous quarter; the chain growth rate was -10.6%, while the previous quarter was a quarter-on-quarter growth. 30.0%. Sales: growth rate decline In the second quarter of 2011, China's steel industry product sales revenue was 1,738.77 billion yuan, a year-on-year increase of 23.0%, the growth rate slowed by 3.0 percentage points from the previous quarter; the chain rose by 6.7%, the growth rate slowed down from the previous quarter by 8.1 percentage point. Inventory: growth slowed down in the second quarter of 2011, due to the decline in raw material iron ore prices, the steel export situation is weakening, and in the downstream industry, the demand for steel products will continue to weaken, the growth rate of finished steel products in the steel industry has been released. Slow, may start a new round of destocking process. As of the end of the second quarter of 2011, the capital occupation of finished steel products was 226.55 billion yuan, a year-on-year increase of 18.2%, and the growth rate slowed by 6.5 percentage points from the previous quarter. Exports: Continued Weakness Recently, the pace of economic recovery in the United States has slowed down, the overseas steel market is in a downturn, and international steel prices are declining. At the same time, due to the rising average price of steel exports, domestic and international spreads have shrunk, and China’s steel exports are in a weak state. The proportion of production continued to decline. After preliminary seasonal adjustment, the export value of steel in the second quarter of 2011 was US$14.56 billion, a year-on-year increase of 48.5%. The year-on-year growth rate was 11.7 percentage points higher than the previous quarter; the chain growth was 42.1%, and the growth rate was 21.6 percentage points higher than the previous quarter. The export growth rate was significantly accelerated by the base. Since mid-June, the domestic steel market has shifted from a narrow range to a full-line decline, and the market has a strong wait-and-see atmosphere. It is expected that downstream demand will remain sluggish in the next few months. The domestic steel market will remain weak, or it will drive down the international steel market. As a result, the domestic and international spreads may continue to narrow, which will inevitably inhibit steel exports. China's steel export situation is still grim. Ex-factory price: downward fluctuation On the one hand, the international steel market is in the downward channel, the domestic steel market maintains a shock consolidation pattern, and the effective demand is weakened. On the other hand, although the growth rate of crude steel production has declined somewhat, it is still at a high level. The basic situation has not changed. Driven by the above factors, in the second quarter of 2011, the ex-factory price of producers in the steel industry rose by 9.5% year-on-year, and the growth rate dropped by 8.2 percentage points from the previous quarter. At present, the situation of iron ore pressure is serious, and there is a downside in the cost of the steel industry. It is expected that domestic steel prices will continue to fall in the third quarter. Profit: low level In the quarter, although China's iron ore import price has declined, it has reduced the profit pressure of the steel industry to a certain extent, but the role of the steel industry's product price and price decline is the dominant factor, making the steel industry profitability level. Reduced. After preliminary seasonal adjustment, the total profit of the steel industry in the second quarter of 2011 was 41.89 billion yuan, a year-on-year growth rate of -13.6%, compared with a year-on-year increase of 25.3%; the chain growth was 5.1%, and the growth rate of the chain was slightly higher than the previous quarter by 3.6. percentage point. The profit margin of the steel industry maintained 2.4% in the previous quarter, far below the national industrial sales profit rate of 6.2%. It is the least profitable industry in China's major industries except oil processing, coking and nuclear fuel processing. Loss: still large and adjusted by the initial season. In the second quarter of 2011, the loss of the loss-making enterprises in the steel industry totaled 5.37 billion yuan, a decrease of 1.99 billion yuan from the previous quarter and an increase of 2.48 billion yuan over the same period of last year. The loss was down from 20.9% in the previous quarter. This quarter's 20.2% is still significantly higher than the 13.5% loss level of all industries. Taxation: Apparently falling back In the second quarter of 2011, the profitability of the steel industry declined, driving the growth rate of total tax revenue to decline. After the initial seasonal adjustment, the total tax revenue of the steel industry in the second quarter of 2011 was 27.87 billion yuan, a year-on-year increase of 0.9%. The year-on-year growth rate slowed down by 23.9 percentage points from the previous quarter; the chain growth rate was -23.3%, and the previous quarter was a year-on-year increase of 24.4. %. According to estimates, random factors have driven the tax expenditure on the steel industry to reduce by 940 million yuan. Employment: Slower growth As the growth rate of steel industry production and sales slows down, steel prices fall, profitability declines, and employment growth in the steel industry slows down. In the second quarter of 2011, the number of employees in the steel industry was 3.208 million, an increase from the previous quarter; the number of employees increased by 6.6% year-on-year, and the growth rate was 0.9 percentage points lower than that of the previous quarter, but still lower than the average industrial scale above the scale. 10.6% growth rate. Investment: The low recovery was driven by the still-increasing urban fixed asset investment. After the initial seasonal adjustment, the fixed assets investment of the steel industry in the second quarter of 2011 was 94.16 billion yuan, a year-on-year increase of 10.5%, and the growth rate was 5.7 percentage points higher than the previous quarter. It is still at a historical low; the chain increased by 111.6%, and the growth rate of the previous quarter was -57.2%. Accounts receivable: continue to improve In the second quarter of 2011, the net receivables of the steel industry was RMB 20.38 billion, a year-on-year increase of 20.2%, and the year-on-year growth rate decreased by 6.3 percentage points from the previous quarter. After calculation, the quarterly receivables turnover days decreased from 10.9 days in the previous quarter to 10.0 days in the current quarter, and the capital turnover continued to improve, and was significantly better than the average turnover days of all industrial 28.5 days of accounts receivable. It shows that the steel industry's asset flow is accelerating and its solvency is further enhanced. Business climate: relatively stable In the second quarter of 2011, the steel industry's prosperity index was 118.5, up 4.3 points from the previous quarter, maintaining the momentum of the last quarter. This shows that steel companies have a relatively stable confidence in the prospects of the steel industry. Industry expectations and recommendations Overall, the current steel industry market demand tends to be sluggish, the steel industry's production and sales growth rate has slowed down, steel product prices fluctuated downward, the steel industry profitability level is at a low level, and steel companies' losses have increased significantly compared with the same period last year. Iron and steel enterprises are also at a relatively high level in the industrial sector, and steel companies are cautious about employment. However, under the overall investment of the whole society, the investment growth rate of the steel industry has rebounded at a low level, and the rate of collection of accounts receivable has continued to accelerate. In the third quarter of 2011, the situation facing the development of the steel industry is more complicated. First, strategic emerging industry investment and other people's livelihood projects have a positive effect on investment, while real estate control measures have inhibited the growth of investment to a certain extent, so investment factors may show a moderate decline. Secondly, the growth rate of consumption of household appliances, automobiles and other products has declined, which has had a certain impact on the growth of manufacturing industries such as automobiles and machinery. With the arrival of the traditional low demand for steel products, the pattern of weak operation in the domestic steel market will be difficult to change in the short term. Thirdly, from the perspective of the external demand market, the steel demand for post-disaster reconstruction in Japan is first driven by the increase in capacity utilization rate in Japan (the capacity utilization rate in Japan before the earthquake is not high), and the scale and progress of reconstruction will affect the foreign steel. Demand, Japan's post-disaster reconstruction may not have a significant impact on China's steel exports; Europe and the United States gradually entered a seasonal summer break, market demand into a dull period. From the micro survey of some steel mills, the export orders for steel from Europe have decreased significantly since May, and some steel mills have zero orders for Europe in June. In addition, the cumulative effect of raising the reserve ratio and raising interest rates has appeared for some time. High financing costs not only affect steel companies, but also affect the investment and production of steel downstream enterprises. Affected by the domestic and international demand situation, China's steel industry may face the situation of poor steel sales and the resulting steel prices are weak, and iron ore prices continue to fall, it is expected to expand the profitability of steel companies. In general, China's steel industry is expected to maintain a moderate decline in the third quarter of 2011, and may step into the “destocking†channel. In the face of complex situations, the steel industry should respond to the following aspects: First, steel companies should pay close attention to market trends and timely adjust and optimize iron ore procurement strategies. When purchasing iron ore, appropriately adjust the proportion of domestic and foreign mineral materials, and more comprehensively consider the factors affecting the iron ore market, and try to control the rhythm of the price of minerals to minimize the cost. Second, iron and steel enterprises should actively participate in the observation of market trends, and try to participate in futures and spot transactions at the same time, in order to make up for losses through the recent market complementarity. In addition, the pattern of the domestic steel distribution industry is changing. Steel companies should try to extend the service chain and do deep processing to meet the diversified and personalized needs of customers. Third, iron and steel enterprises should speed up the "going out" pace, better use of "two markets" and "two kinds of resources" will become an inevitable choice for China's steel industry to further enhance resource support capabilities and international competitiveness. In the process of development, China's steel enterprises should pay more and more attention to the establishment of factories in areas with resources and markets overseas. Conditional enterprises should regard overseas layout as an important part of corporate strategic development. At the same time, the export of high-end products and services should be replaced by the export of low-end products. Notes: 1 The steel industry refers to the ferrous metal smelting and rolling processing industry in the national economic industry classification. The statistical scope of this report is nearly 6,400 industrial enterprises above designated size in the industry. In 22000, the warning signs of the steel industry were basically in the green light area, which was relatively stable, so it was set as the base year of the China Economic and Steel Industry Climate Index. 3 According to the calculation method of the climate warning index system, the composition indicators of the industry prosperity index and the industry early warning index should be adjusted seasonally to eliminate the influence of seasonal factors on the data. Therefore, when the industry climate index and early warning index release the current data, the previous data will also be adjusted. . 4 Seasonal factors refer to the impact of seasonal changes on the data. For example, the market sales of cold drinks vary with the temperature of the four seasons year after year. 5 Random factors are also called irregularities, such as the impact of new policy implementation, macro-control, natural disasters and other factors on the data. 6 Reversal indicators, also called reverse indicators, have a negative effect on the industry's operating conditions. The lower the indicator value, the better the industry situation, and vice versa. 7 Preliminary seasonal adjustment refers to only eliminating the influence of holiday factors such as the Spring Festival, and does not remove the influence of irregular factors.Loader Parts,Track Loader Parts,Case Loader Parts,Skid Loader Parts

JINING SHANTE SONGZHENG CONSTRUCTION MACHINERY CO.LTD , https://www.sdkomatsugenuineparts.com